Earnings are anticipated to present perception into the consequences of inflation and influence of the Fed’s anticipated coverage tightening.

U.S. equities declined in the beginning of a busy week for company earnings as buyers are intently watching outcomes for insights into the impact of inflation and shopper spending because the Federal Reserve steps up coverage tightening.

The S&P 500 and Nasdaq 100 slipped greater than 1% after Monday’s uneven positive aspects. Common Electrical Co. slid after saying 2022 revenue can be close to the low finish of forecasts on provide chain woes. Twitter Inc. fell after Elon Musk sealed a deal to purchase the social-media platform. In the meantime, Treasuries, the greenback and oil costs all rose, with West Texas Intermediate futures rebounding from a 1.5% drop earlier within the session.

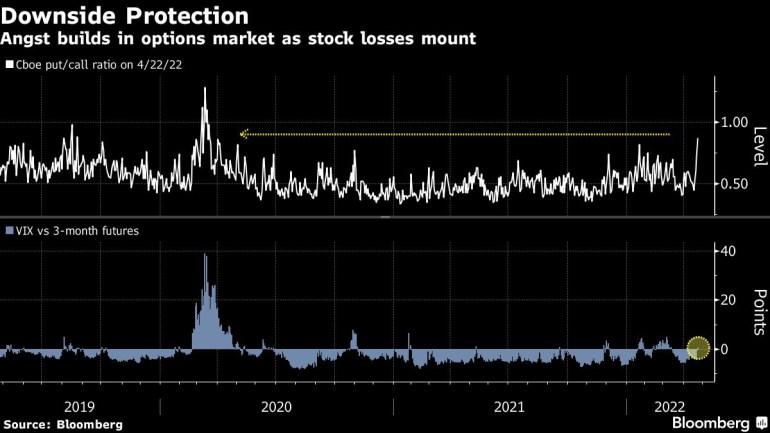

The prospect of slower financial enlargement alongside persistent inflation is resulting in a febrile temper in markets. The panoply of dangers spans the pandemic, supply-chain disruptions, Fed tightening and Russia’s grinding conflict in Ukraine. The seek for portfolio buffers within the U.S. is clear within the highest relative value of loss-protecting put contracts in two years.

“It’s a query of what’s financial coverage going to seem like and it’s tremendous unknown,” Nancy Davis, chief funding officer at Quadratic Capital Administration LLC, mentioned on Bloomberg Tv.

U.S. company earnings are offering some solace for fairness bulls — near 80% of companies have crushed revenue expectations together with GE, United Parcel Service Inc. and Pepsico Inc. Nonetheless, disappointing earnings forecasts, together with these from JetBlue Airways Corp., are weighing on shares. Outcomes from Microsoft Corp., Google guardian Alphabet Inc. and Visa Inc. are nonetheless to return.

“This would be the busiest week of experiences for the primary quarter earnings season,” Artwork Hogan, chief market strategist at Nationwide Securities, mentioned in a notice. “This could present buyers a possibility to shift their focus from the macro headwinds like inflation, the Fed, China lockdowns, and the conflict in Ukraine, and permit them to disseminate company outcomes to determine if applicable valuations have been ascribed within the wake of the markets’ April drawdown.”

China Enhance

Shares in Europe climbed as China’s pledge to spice up monetary-policy help for its Covid-hit economic system lifted sentiment, whereas merchants additionally eyed a raft of earnings experiences from a few of the area’s largest corporations.

The Stoxx 600 Europe rebounded from a six-week low, with Novartis AG and UBS Group AG among the many largest index movers after optimistic first-quarter experiences. Primary sources led the advance, buoyed by earnings beats from paper maker UPM-Kymmene Oyj and ball-bearing producer SKF AB.

Apart from vowing extra help, the Individuals’s Financial institution of China additionally mentioned it is going to promote wholesome and secure improvement in monetary markets. Most of Beijing is being examined for the virus, fanning fears of an unprecedented lockdown there that would drag on world development.

An Asia-Pacific fairness index eked out a climb for the primary time in 4 periods amid a 3% leap in expertise shares in Hong Kong. Mainland Chinese language bourses dipped however prevented the type of plunge witnessed Monday. The yen pushed greater amid brief masking.

Fears over the lockdowns have weighed closely on market sentiment, however considerations over the inflationary strain could also be overblown, Dennis DeBusschere, founding father of 22V Analysis, mentioned in a notice.

“There are not any compounding provide chain pressures from different necessary provide chain nations like in 2021,” he mentioned. “There's softer shopper demand normally, service spending is recovering (moderating items spending) and the USD is transferring greater.”

What would be the 2022 peak in U.S. 10-year yields and through which quarter will it occur? And what rock or pop tune greatest encapsulates Fed financial coverage? Become involved on this week’s MLIV Pulse survey by clicking right here. Participation takes one minute and is nameless.

Occasions to observe this week:

- Tech earnings embrace Alphabet, Meta Platforms, Amazon, Apple

- EIA oil stock report, Wednesday

- Australia CPI, Wednesday

- Financial institution of Japan financial coverage resolution, Thursday

- U.S. 1Q GDP, weekly jobless claims, Thursday

- ECB publishes its financial bulletin, Thursday

A number of the principal strikes in markets:

Shares

- The S&P 500 fell 1% as of 9:50 a.m. New York time

- The Nasdaq 100 fell 1.6%

- The Dow Jones Industrial Common fell 0.9%

- The Stoxx Europe 600 rose 0.3%

- The MSCI World index fell 0.6%

Currencies

- The Bloomberg Greenback Spot Index rose 0.2%

- The euro fell 0.4% to $1.0673

- The British pound fell 0.5% to $1.2676

- The Japanese yen rose 0.8% to 127.09 per greenback

Bonds

- The yield on 10-year Treasuries declined eight foundation factors to 2.74%

- Germany’s 10-year yield declined two foundation factors to 0.82%

- Britain’s 10-year yield declined three foundation factors to 1.81%

Commodities

- West Texas Intermediate crude rose 1.1% to $99.61 a barrel

- Gold futures rose 0.6% to $1,907.30 an oz.

–With help from Joanna Ossinger and Robert Model.

Post a Comment